How a Cash Sale Stops Foreclosure Before Auction

TL;DR:

- A cash sale pays off your mortgage before the foreclosure auction, stopping the legal process. It is the fastest and most reliable method to prevent foreclosure, often closing within two weeks. Acting early and contacting your lender promptly increases your chances of saving your home and protecting your equity.

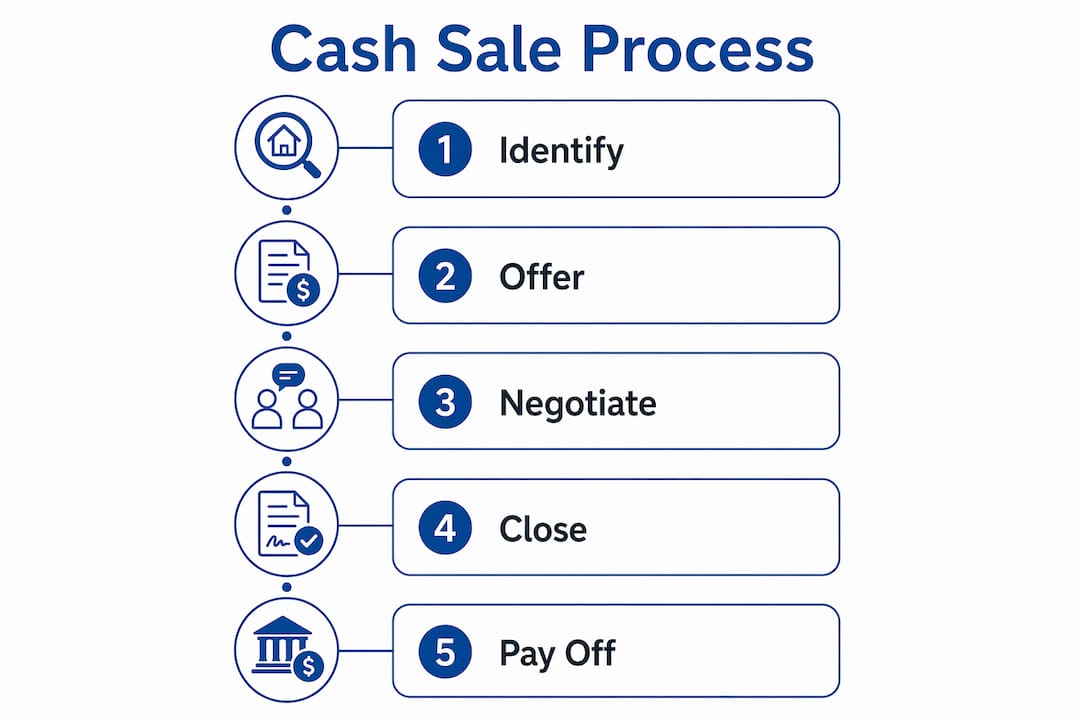

A cash sale stops foreclosure by paying off your mortgage lender in full before the foreclosure auction date, which legally cancels the lender’s claim against your property. The industry term for this strategy is a “pre-foreclosure sale,” and it is one of the most reliable foreclosure prevention strategies available to homeowners in financial distress. Under 2026 CFPB regulations, lenders cannot begin formal foreclosure until you are at least 120 days behind on payments, giving you a critical window to act. Understanding how cash sale stops foreclosure means understanding that timing, not price, is the deciding factor.

How does a cash sale stop foreclosure?

A cash sale cancels foreclosure by generating enough proceeds at closing to pay off your outstanding mortgage balance before the auction date. When the title company disburses funds to your lender at closing, the lender cancels the foreclosure filing and releases the lien on your property. No auction happens. No forced sale. The process ends on your terms.

The speed of a cash transaction is what makes this work. Cash buyers close in 7–14 days, compared to 30–90 days for traditional listings. That difference is the margin between saving your equity and losing your home at auction.

What is the foreclosure timeline and where does a cash sale fit in?

Foreclosure follows a predictable legal sequence, and knowing each stage tells you exactly when a cash sale can intervene.

- Missed payments (days 1–120): Your lender records late payments and begins contacting you. No formal foreclosure action can begin during this period under CFPB rules.

- Notice of default (day 120+): The lender files a formal notice, which is the legal start of foreclosure. This is public record.

- Pre-auction period: Depending on your state, this window lasts anywhere from a few months to over a year. Judicial foreclosure states like Michigan typically allow more time than nonjudicial states.

- Foreclosure auction: The property sells to the highest bidder. Once the auction is confirmed, your options narrow sharply.

- Post-auction period: A handful of states, including North Carolina, allow a 10-day upset bid period after auction, but relying on this window is risky and unreliable.

The pre-auction period is where a cash sale does its best work. The CFPB’s 120-day preforeclosure window gives you roughly four months from your first missed payment to arrange a controlled sale. State timelines vary widely, so knowing your state’s specific schedule is critical to building a realistic plan.

Pro Tip: Contact your state’s housing finance agency or a HUD-approved housing counselor to get the exact foreclosure timeline for your state. This one call can tell you how many days you actually have.

How does a cash sale legally stop foreclosure compared to other options?

A cash sale works because it produces an immediate, guaranteed payoff to your lender. There are no financing contingencies, no appraisal requirements, and no underwriting delays. Removing these contingencies eliminates the risk of a deal falling apart days before your auction date, which is exactly what happens with many traditional sales.

Cash sale vs. short sale

A short sale requires your lender to approve a sale price below what you owe. That approval process takes weeks or months, and there is no guarantee the lender agrees. A short sale drops your credit score by 50–150 points. A completed foreclosure drops it by 200–300 points. A cash sale that closes before auction avoids the foreclosure mark on your credit entirely, which is the best possible outcome.

Cash sale vs. deed in lieu of foreclosure

A deed in lieu transfers your property directly to the lender to cancel the debt. It avoids auction but leaves you with nothing. A cash sale, by contrast, pays off the mortgage and returns any remaining equity to you. If your home is worth more than you owe, a cash sale is the only option that puts money back in your pocket.

Lenders also prefer a voluntary sale to a forced auction because it simplifies asset recovery and typically recovers more funds. A credible cash offer on the table can motivate a lender to pause or extend the foreclosure sale date, buying you the time you need to close.

Pro Tip: Present your lender’s loss mitigation department with a signed purchase agreement from a cash buyer. A real offer in hand gives the lender a concrete reason to delay the auction.

What steps do homeowners need to take to use a cash sale to stop foreclosure?

Acting fast and in the right sequence is what separates homeowners who stop foreclosure from those who run out of time.

-

Call your lender’s loss mitigation department immediately. Ignoring lender calls is the single most damaging mistake you can make. Lenders often offer repayment plans or temporary extensions that can buy you critical extra weeks to complete a sale.

-

Request a payoff quote. Ask your lender for the exact amount needed to satisfy your mortgage at closing. This number changes daily due to interest, so get an updated figure once you have a buyer.

-

Find a reputable cash buyer who closes fast. Look for buyers with a documented track record of closing in 7–14 days. Verify proof of funds before signing anything. Sell Dave Your House, for example, provides a fair cash offer within 24 hours and can close in as little as seven days.

-

Gather your key documents. You will need your mortgage statement, the payoff quote, your deed, and any foreclosure notices you have received. Your title company will coordinate the rest.

-

Close before the auction date. The title company disburses the payoff to your lender at closing. The lender then cancels the foreclosure filing. Your sale proceeds, minus the payoff and closing costs, come to you.

-

Avoid common delays. Do not wait for a “better offer.” Do not skip lender calls. Do not assume you have more time than you do. Every day of delay shrinks your options.

Pro Tip: Ask your cash buyer to provide a proof-of-funds letter on day one. Lenders respond faster and more favorably when they see a real buyer with real money ready to close.

Maintaining open communication with your lender throughout this process is not optional. Lenders who see a homeowner actively working toward a solution are far more likely to grant extensions or pause proceedings than lenders dealing with silence.

What are the benefits and limitations of cash sales as foreclosure prevention strategies?

A cash sale is not a perfect solution for every homeowner, but for most people facing imminent foreclosure, it is the strongest option available.

Benefits

- Speed: Cash sales close in 7–14 days, fast enough to stop foreclosure even late in the timeline.

- No repairs required: Cash sales avoid costly repairs and the delays that come with them, keeping your closing on schedule.

- No commissions or hidden fees: You keep more of your sale proceeds, which matters when every dollar counts toward paying off your mortgage.

- Equity protection: Selling before auction preserves whatever equity you have built. A forced auction sale almost always recovers less than market value.

- Credit protection: Closing a cash sale before foreclosure is finalized prevents the foreclosure from appearing on your credit report, protecting your financial future.

Limitations

- Price: Cash buyers typically offer below full market value. The trade-off is speed and certainty, which outweigh a higher price that arrives too late.

- Not viable post-auction: Once the foreclosure auction is confirmed and the redemption period (if any) has passed, a cash sale can no longer stop the process.

- Equity must cover the payoff: If you owe more than your home is worth, a cash sale alone may not satisfy the lender. In that case, a short sale or negotiated settlement may be necessary alongside the cash transaction.

- State law variations: Your state’s foreclosure timeline and redemption rights directly affect how much time you have and what options remain open.

The core principle holds: timing matters more than price. A quick cash sale at a slightly lower price preserves far more equity than waiting for a higher offer that arrives after the auction gavel falls.

Key Takeaways

A cash sale stops foreclosure by paying off the lender at closing before the auction date, making it the fastest and most reliable foreclosure prevention strategy available to homeowners.

| Point | Details |

|---|---|

| Act within the 120-day window | The CFPB gives lenders 120 days before filing foreclosure, making early action your strongest advantage. |

| Cash closes in 7–14 days | Cash buyers close far faster than traditional listings, giving you a realistic path to stop the auction. |

| Call your lender first | Loss mitigation departments can pause proceedings when presented with a signed cash purchase agreement. |

| Cash sale protects equity and credit | Closing before auction preserves your equity and prevents a foreclosure from appearing on your credit report. |

| Price matters less than timing | A slightly lower cash offer accepted today saves more equity than a higher offer that arrives after the auction. |

What I’ve learned about timing and lender communication in foreclosure situations

The homeowners who successfully stop foreclosure share one trait: they act before they feel ready. The ones who lose their homes almost always waited, either hoping the situation would resolve itself or assuming they had more time than they did.

Lenders are not the enemy in this process. Loss mitigation departments exist specifically to avoid the cost and complexity of a forced auction. When you call them with a real cash offer in hand, the conversation changes. They have a concrete path forward, and most will work with you to make it happen.

What surprises many homeowners is how much flexibility lenders actually have. A credible purchase agreement from a qualified cash buyer can pause a scheduled auction. That is not a guarantee, but it is a real and documented outcome that happens regularly. The key word is “credible.” A vague promise to sell does nothing. A signed contract with proof of funds does a great deal.

My honest observation after years of watching these situations play out: the homeowners who treat a cash sale as a last resort almost always wait too long. The homeowners who treat it as a first-line strategy, one option among several to evaluate immediately, consistently get better outcomes. Seek professional advice early, whether from a HUD-approved counselor, a real estate attorney, or an experienced cash buyer. The earlier you get informed, the more options you have.

— Real Estate Team

How Sell Dave Your House helps you stop foreclosure fast

If you are facing foreclosure in the Detroit area, Sell Dave Your House offers a direct path forward. With over 16 years of experience and a process built for speed, Sell Dave Your House provides a fair cash offer within 24 hours and can close in as little as seven days.

There are no repairs to make, no agent commissions to pay, and no financing delays to worry about. Sell Dave Your House serves homeowners across Detroit, Harper Woods, Hazel Park, and surrounding communities. If your auction date is approaching, the right move is to get a cash offer today and let the closing process do the work of stopping foreclosure before it is too late.

FAQ

How quickly can a cash sale stop foreclosure?

A cash sale can stop foreclosure in as little as 7–14 days from the time you accept an offer. The closing process pays off your lender directly, and the lender cancels the foreclosure filing upon receipt of funds.

What happens to my equity when I sell for cash before foreclosure?

Any proceeds above your mortgage payoff and closing costs come to you. Selling before auction is the only way to recover equity, since forced auction sales typically recover less than market value.

Can I sell my house after foreclosure proceedings have started?

Yes. You can sell your house at any point before the foreclosure auction is confirmed. Once you have a signed purchase agreement and a closing date before the auction, the sale legally halts the foreclosure process.

Does a pre-foreclosure cash sale hurt my credit?

A completed cash sale before foreclosure does not add a foreclosure record to your credit report. A foreclosure, by contrast, drops your credit score by 200–300 points and stays on your report for seven years.

What if I owe more than my home is worth?

If your mortgage balance exceeds your home’s value, a standard cash sale may not cover the full payoff. In that case, you may need to negotiate a short sale with your lender, where the lender agrees to accept less than the full balance owed.