How Cash Offers Bypass Repair Contingencies Fast

TL;DR:

- Cash offers bypass repair contingencies by removing lender requirements, allowing homeowners to sell as-is quickly. They close faster, with fewer risks of deal collapse, but tend to be for below-market prices due to repair cost deductions. Proper preparation, such as clearing titles and honest disclosure, can maximize these benefits for distressed sellers.

Cash offers bypass repair contingencies by removing the lender’s authority to demand property fixes before funding. When a buyer pays cash, there is no FHA, VA, or USDA loan program requiring your home to meet strict health, safety, or habitability standards. That single fact changes everything for homeowners in financial distress. You can sell your house exactly as it sits, skip the repair bills, and close in as little as 7 days. This guide explains how the process works, what to watch out for, and how to use it to your advantage.

How cash offers bypass repair contingencies

Cash offers bypass repair contingencies because they remove the lender’s authority to demand repairs as a condition for funding. No lender means no one standing between you and the closing table, insisting your roof, electrical panel, or foundation meet a specific standard before the deal can proceed. The industry term for this is an “as-is sale,” and it is the defining feature of cash transactions in real estate.

The mechanics are straightforward. A cash buyer uses their own funds. Because no bank is involved, no lender inspections are triggered, and no repair demands follow. The buyer accepts the property in its current condition, defects and all. You disclose what you know, sign the paperwork, and move forward.

This matters most when you are facing foreclosure, dealing with an inherited property in poor condition, or simply cannot afford to spend $15,000 fixing a house before selling it. The as-is sale is not a workaround. It is a legitimate, widely used path that protects sellers from the repair spiral that derails so many traditional home sales.

What are repair contingencies and why do lenders require them?

A repair contingency is a clause in a purchase contract that makes the sale conditional on specific repairs being completed before closing. Lenders require these clauses because they are protecting their investment, not yours.

Government-backed loan programs impose the strictest standards. FHA loans require properties to meet the U.S. Department of Housing and Urban Development’s Minimum Property Standards. VA loans require a VA appraiser to certify the home is safe, sound, and sanitary. USDA loans carry similar habitability requirements. FHA, VA, and USDA loans trigger mandatory pre-sale repairs that can cost thousands and take weeks to complete.

Conventional loans backed by Fannie Mae or Freddie Mac also require appraisals. If an appraiser flags a structural issue, a broken HVAC system, or a damaged roof, the lender can require repairs before approving the mortgage. Here is what that process typically looks like for a seller:

- A buyer’s inspector identifies defects during the inspection period.

- The buyer submits a repair request or requests a price reduction.

- The lender’s appraiser independently flags additional issues.

- The seller must fix the problems, reduce the price, or watch the deal fall apart.

- Closing gets pushed back by weeks while contractors are scheduled and work is verified.

Each step adds time, cost, and uncertainty. For a homeowner already under financial pressure, this process can feel impossible to manage.

Why does removing the lender eliminate repair demands?

The lender is the source of repair requirements in financed sales. Remove the lender, and the requirement disappears entirely. Cash transactions close faster on average, typically within 7–21 days, compared to conventional sales that can take 30–60 or more days. That speed comes directly from cutting out the underwriting, appraisal, and inspection chain.

Cash buyers accept responsibility for all defects, including structural issues, broken systems, and cosmetic damage. Sellers disclose known defects but are not obligated to fix anything before the sale closes. The buyer prices their offer to account for those defects, which is why cash offers often come in below full market value. That tradeoff is real, and it is worth understanding clearly.

The other major benefit is deal certainty. Fewer contingencies mean fewer exit points for the buyer. Cash offers reduce deal cancellations because there is no financing contingency that can collapse if the buyer’s mortgage falls through. For a homeowner who needs a guaranteed close, that reliability is often worth more than squeezing out a higher sale price.

Key advantages of bypassing repair requirements through cash sales:

- No lender-mandated inspection or repair list

- No appraisal that can derail the deal

- No financing contingency that can collapse at the last minute

- Closing in 7–21 days instead of 30–60 or more

- No out-of-pocket repair costs before closing

Practical strategies for optimizing your cash offer sale

Avoiding repair negotiations does not mean doing nothing to prepare. The sellers who close fastest are the ones who handle the non-repair obstacles early.

1. Clear your title before you list. Title issues, unpaid liens, and unresolved probate are the most common reasons cash sales get delayed. Clearing title and liens early allows 7–21 day closings to happen on schedule. Pull a title report as soon as you decide to sell, and address anything that shows up immediately.

2. Disclose all known defects honestly. Every state requires sellers to disclose material defects. This is not optional, and it protects you legally. A cash buyer already expects problems. Honest disclosure builds trust and prevents the buyer from backing out later over something you failed to mention.

3. Understand the pricing reality. Cash buyers price properties to account for visible defects and assumed risks, which results in lower offers than fully repaired homes. This is not a flaw in the process. It reflects the genuine cost the buyer is taking on. Knowing this in advance helps you evaluate offers without feeling blind sided.

4. Get multiple offers. Do not accept the first cash offer you receive. Contact several cash buyers and compare. The spread between offers can be significant, and you have more negotiating room than you might expect even without repairs as a lever.

5. Work with a buyer who has a clear track record. Ask for proof of funds and references from past sellers. Speed and certainty only matter if the buyer actually closes.

Pro Tip: Use a home selling checklist to track title clearance, disclosure documents, and closing logistics. Sellers who stay organized close faster and with fewer surprises.

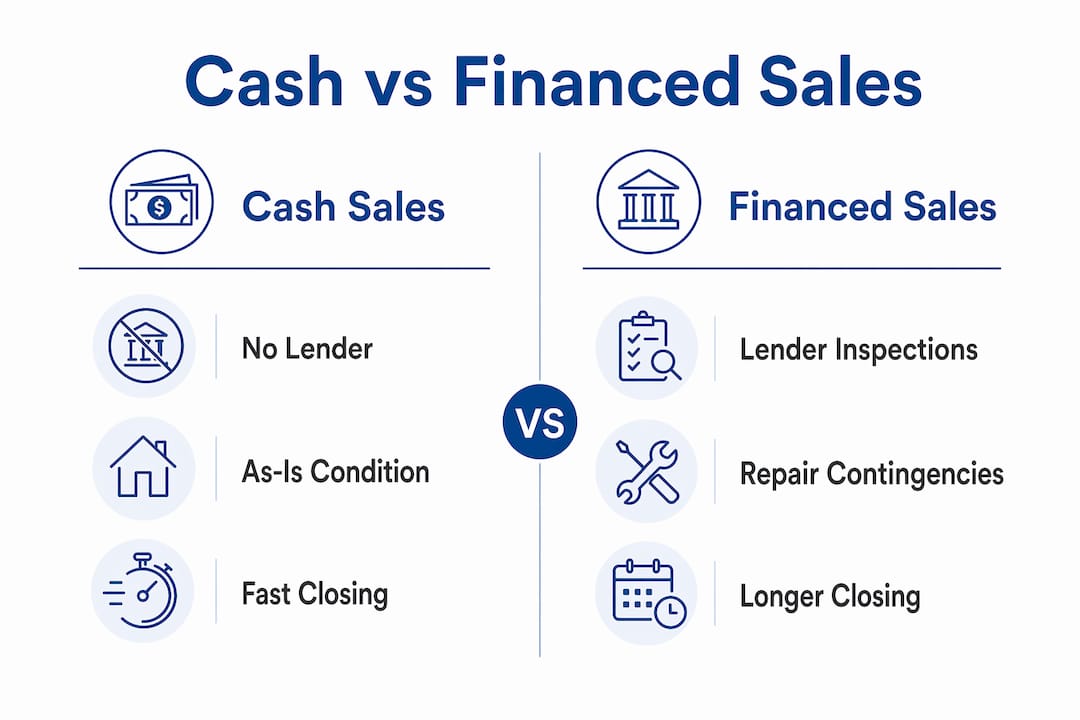

Cash sales vs. traditional financed sales: what are the real tradeoffs?

The decision to accept a cash offer versus waiting for a financed buyer comes down to your specific situation. Speed and certainty favor cash. Maximum sale price often favors waiting for a financed buyer, assuming your home can pass inspection.

Homeowners with urgent financial hardship, inherited properties, or major structural damage benefit most from cash offers that skip repair requirements and close quickly. These sellers typically lack the time or funds to perform repairs and need a guaranteed result.

Here is how the two paths compare across the factors that matter most to distressed sellers:

| Factor | Cash sale | Traditional financed sale |

|---|---|---|

| Closing timeline | 7–21 days | 30–60+ days |

| Repair requirements | None | Lender and appraiser mandated |

| Deal fall-through risk | Low | Higher due to financing and inspection |

| Sale price | Below market value | Closer to full market value |

| Out-of-pocket costs | Minimal | Repairs, staging, agent commissions |

| Certainty of close | High | Moderate |

The financial gap between a cash offer and a financed offer is real but often smaller than sellers expect once you subtract repair costs, agent commissions, carrying costs during a longer sale, and the risk of a deal falling through entirely. For a homeowner facing foreclosure or an unmanageable property, the certainty of a fast cash close frequently outweighs the price difference.

Traditional sales make more sense when your home is in good condition, you have time to wait, and you want to maximize your net proceeds. If any of those three conditions is missing, the benefits of cash offers become harder to ignore.

Key Takeaways

Cash offers bypass repair contingencies by eliminating lender involvement, allowing homeowners to sell as-is in 7–21 days with no repair costs, no appraisal risk, and significantly lower deal fall-through rates.

| Point | Details |

|---|---|

| Lenders drive repair demands | FHA, VA, USDA, and conventional loans all require property condition standards that cash sales skip entirely. |

| As-is sales are legally sound | Sellers disclose known defects but are not required to fix anything before a cash sale closes. |

| Speed is the core advantage | Cash transactions close in 7–21 days versus 30–60 or more days for financed sales. |

| Expect below-market offers | Cash buyers price in repair costs, so offers run lower than fully repaired comparable homes. |

| Title clearance is critical | Resolving liens and probate early is the single most effective way to protect your closing timeline. |

Why I think cash offers are underrated for distressed sellers

Most articles on this topic focus on the price gap between cash and financed offers. That framing misses the point for homeowners in real distress.

When you are three months behind on your mortgage, facing a foreclosure filing, or holding an inherited property you cannot afford to maintain, the question is not “How do I get the highest price?” The question is “How do I get out of this situation without it getting worse?” Those are fundamentally different problems, and they require different solutions.

The speed and certainty of a cash sale are not just conveniences. They are the difference between stopping a foreclosure and losing the house entirely. They are the difference between settling an estate in weeks and dragging it out for months while carrying costs pile up. I have seen sellers walk away from cash offers because they were fixated on a number they saw on Zillow, only to watch a financed deal collapse three weeks before closing because the buyer’s lender flagged a foundation crack.

My honest advice: do your market research, get multiple offers, and understand what your home would realistically net after repairs, commissions, and carrying costs in a traditional sale. When you run those numbers honestly, the cash offer gap usually shrinks. And the certainty never does.

One caution worth stating clearly: not every cash buyer operates with integrity. Verify proof of funds. Check references. A legitimate buyer will not pressure you to sign before you have had time to review the contract.

— Real Estate Team

Sell Dave Your House makes the as-is process simple

If you are a homeowner in the Detroit area dealing with financial pressure, an inherited property, or a house that needs more repairs than you can handle, Sell Dave Your House offers a direct path forward.

With over 16 years of experience buying homes for cash, Sell Dave Your House delivers a fair cash offer in Detroit within 24 hours and can close in as little as seven days. There are no repair requirements, no agent commissions, and no hidden fees. The team handles title and closing logistics so you are not left managing paperwork alone. Whether you are in Detroit, Harper Woods, or the surrounding metro area, the process is the same: get your offer, review it with no obligation, and close on your schedule.

FAQ

What exactly is a repair contingency in a home sale?

A repair contingency is a contract clause that makes the sale conditional on specific repairs being completed before closing. Lenders require these clauses to protect the value of the property securing their loan.

Why do cash offers not require repairs?

Cash sales remove lender requirements entirely because no bank is funding the purchase. Without a lender, there is no FHA, VA, or USDA standard to meet, and no appraiser to flag defects.

Will I get full market value with a cash offer?

Cash buyers typically offer below full market value because they factor repair and renovation costs into their price. The net difference often narrows once you subtract repair costs, commissions, and carrying costs from a traditional sale.

How fast can a cash sale actually close?

Cash transactions close in 7–21 days on average when title is clear. Sellers who resolve liens and probate issues before accepting an offer close at the faster end of that range.

Do I still need to disclose defects in a cash as-is sale?

Yes. State disclosure laws apply regardless of sale type. Sellers must disclose known defects honestly, but they are not required to repair them before closing in a cash transaction.