Relocation Home Sale Process: A Homeowner’s Guide

TL;DR:

- The relocation home sale process involves two separate transactions that protect homeowners from tax liabilities and double mortgages. A relocation management company purchases the home from the owner at market value and then resells it to an outside buyer, following IRS rules. Most programs, like the Buyer Value Option, help homeowners sell quickly and cost-effectively while maintaining legal and tax compliance.

The relocation home sale process is defined as a structured series of steps where a relocation management company (RMC) helps a homeowner sell their property during a job-related move, using legal frameworks like the Buyer Value Option (BVO) to manage costs and taxes. Most homeowners facing a job transfer don’t realize this process involves two separate real estate transactions, not one. Understanding each step protects you from unexpected tax bills, double mortgage payments, and costly delays. This guide walks you through every phase, from listing your home to closing, so you can move forward with confidence.

What is the relocation home sale process, step by step?

The relocation home sale process follows a clear sequence. Each step involves a specific party, and knowing who does what prevents costly mistakes.

-

You list your home. Your employer’s RMC assigns a Realtor to help you market the property. Relocation programs typically include Realtor marketing assistance, buyer screening, and handling of legal documentation to ease the sale.

-

An outside buyer makes an offer. A buyer from the open market submits an offer on your home. You review it and, if acceptable, signal your intent to accept.

-

The relocation company purchases your home. Instead of you selling directly to the buyer, the RMC steps in and buys your home at the buyer’s offered price. This is the BVO in action.

-

The RMC resells to the outside buyer. The relocation company then completes a separate transaction, selling the home to the original outside buyer. These are two legally distinct contracts, not one.

-

You receive your proceeds and relocate. You get paid by the RMC and can focus entirely on your move, free from the burden of managing a pending sale from another city.

The reason for two separate transactions is not bureaucratic. IRS Revenue Ruling 2005-74 governs this structure, allowing the sale benefits to be treated as business expenses rather than taxable income to you. Without this structure, your employer’s financial assistance could be counted as income, triggering a significant tax bill.

Pro Tip: Never communicate directly with the outside buyer about price or terms after the RMC enters the picture. Direct contact between you and the buyer can collapse the legal separation the IRS requires, turning your employer’s assistance into taxable income.

Timeline matters here. Most BVO transactions close within 60 to 90 days of listing, though markets vary. Starting the process early, ideally before your official transfer date, gives you the most flexibility.

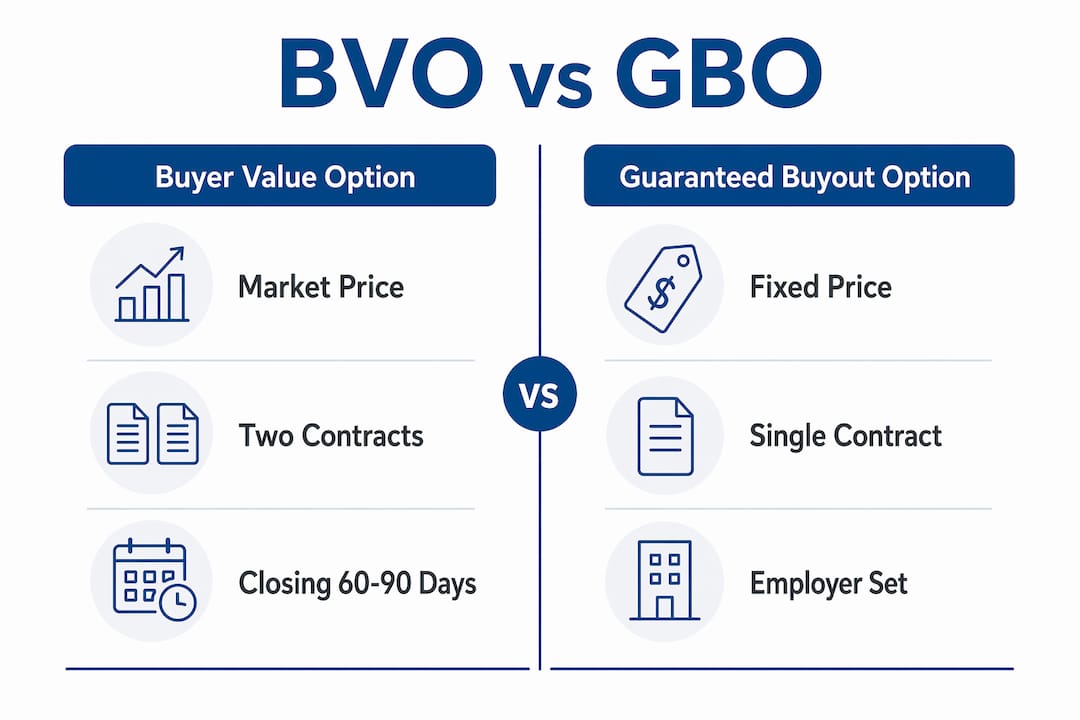

What is the difference between BVO and GBO?

Two programs dominate employer-sponsored home sale assistance: the Buyer Value Option and the Guaranteed Buyout Option (GBO). They solve the same problem differently, and the distinction affects both your financial outcome and your employer’s cost.

The BVO is the most common employer-sponsored program. You find a buyer, the RMC purchases your home at that buyer’s price, and then resells it to the buyer in a separate transaction. The price is set by the market, not by a formula. This protects your employer from overpaying and keeps the transaction tax-efficient for you.

The GBO works differently. Your employer locks in a purchase price for your home regardless of what the market offers. If your home sits unsold, the employer buys it at the agreed price anyway. Employers prefer BVO over GBO because BVO uses market pricing and reduces the risk of holding unsold home inventory. GBO is a safety net employees appreciate, but it carries real financial risk for the company.

| Feature | BVO | GBO |

|---|---|---|

| Price basis | Outside buyer’s market offer | Fixed price set by employer |

| Employee risk | Moderate (must find a buyer) | Low (price is guaranteed) |

| Employer risk | Low (market-driven) | Higher (may buy at above-market price) |

| Tax treatment | Business expense, not employee income | Business expense, not employee income |

| Most common use | Standard corporate relocation | Executive or high-value packages |

Both options protect you from carrying two mortgages during the move, which is one of the most stressful financial risks in any relocation. Removing that risk also improves your willingness to accept the transfer in the first place.

Pro Tip: If your employer offers a choice, ask your RMC to run a market analysis before deciding. In a slow market, a GBO may protect you from a low offer. In a strong market, a BVO typically nets you more.

The RMC pays commissions and closing costs upfront and bills them to your employer as business expenses. This keeps those costs off your personal tax return entirely.

What are the real costs of a relocation home sale?

Relocation home sales carry real costs, and knowing the numbers helps you plan without surprises.

Standard U.S. domestic relocation packages range from $15,000 to $75,000. Adding a BVO program brings the total to approximately $93,000 per move. That figure covers Realtor fees, marketing, legal documentation, and the RMC’s administrative costs.

Closing costs alone can consume roughly 8% of your home’s value. On a $300,000 home, that’s $24,000 in closing costs. In a traditional sale, you would absorb most of that. In a BVO or GBO program, your employer absorbs it through the RMC.

Key cost categories to understand:

- Realtor commissions: Typically 5–6% of the sale price, paid by the RMC and billed to your employer.

- Closing costs: Title insurance, transfer taxes, attorney fees, and recording fees, totaling roughly 8% of home value.

- RMC administrative fees: Charged to the employer for coordinating the transaction.

- Gross-up costs: If benefits are taxable, employers may gross up your pay to cover the tax. BVO programs are specifically structured to avoid this.

Mid-level professional relocation packages range from $15,000 to $35,000. Executive packages can exceed $90,000 when home sale assistance and family support are included. Your package tier determines how much of the home sale process your employer covers.

Understanding home sale proceeds planning before you list helps you set realistic expectations for what you’ll net after the RMC transaction closes.

Practical tips for selling your home during relocation

Moving and selling a house at the same time is manageable when you follow a clear plan. These practices reduce friction and protect your financial outcome.

Align your timeline early. Contact your RMC the moment you receive your transfer notice. Delays in starting the home sale process compress your timeline and reduce your negotiating room.

Prepare your home before listing. Buyers in relocation sales are often corporate-sponsored and move quickly. A clean, well-presented home attracts faster offers. If repairs feel overwhelming, selling as-is is a legitimate option that eliminates the repair burden entirely.

Keep the two transactions legally separate. Employees must sign two legally distinct contracts during BVO sales to avoid IRS penalties. Never negotiate directly with the outside buyer after the RMC takes ownership. Your RMC and Realtor handle all buyer communication from that point forward.

Document everything. Keep records of all RMC correspondence, offer letters, and closing statements. These documents matter if the IRS ever questions the tax treatment of your relocation benefits.

Communicate clearly with your employer. Ask your HR department exactly what your relocation package covers. Packages vary widely by company and employee level. Knowing your coverage prevents you from paying out of pocket for costs your employer would have covered.

Pro Tip: Ask your RMC for a written timeline at the start of the process. A clear schedule with milestones, listing date, offer deadline, and closing target, keeps everyone accountable and reduces last-minute surprises.

Selling your house fast matters most when your start date at the new job is fixed. The more lead time you give the process, the better your outcome.

Key Takeaways

The relocation home sale process protects homeowners from tax liability and double mortgage payments through a structured two-transaction framework governed by IRS Revenue Ruling 2005-74.

| Point | Details |

|---|---|

| Two separate transactions | BVO requires two legally distinct contracts to keep employer assistance off your tax return. |

| BVO vs. GBO choice | BVO uses market pricing; GBO locks in a fixed price regardless of market conditions. |

| Real cost range | Full relocation packages with BVO can total approximately $93,000, mostly absorbed by employers. |

| Closing cost exposure | Closing costs consume roughly 8% of home value; RMC programs shift this cost to the employer. |

| Timeline discipline | Starting the home sale process early, before your transfer date, gives you the most flexibility and best offers. |

What I’ve learned from watching homeowners navigate relocation sales

Most homeowners walk into a relocation home sale thinking it works like a regular sale with extra paperwork. It doesn’t. The legal separation between the two transactions is not a formality. It is the entire mechanism that keeps your employer’s assistance from becoming a taxable windfall on your W-2.

The tax nuance surprises people every time. I’ve seen homeowners communicate directly with outside buyers after the RMC stepped in, thinking they were being helpful. That single mistake collapsed the legal separation and triggered a gross-up situation that cost the employer thousands and created confusion for the employee at tax time. The rule is simple: once the RMC is involved, you step back from buyer contact entirely.

The other lesson is about timing. Homeowners who start the process late, often because they’re focused on the new job, end up accepting lower offers or carrying two mortgages for a month or two. That financial pressure is avoidable. Your RMC can only work as fast as you give them room to work.

Early planning and clear communication with your RMC are not just good habits. They are the difference between a smooth relocation and a stressful one that follows you into your new role.

— Real Estate Team

Sell Dave Your House: a faster path for Detroit homeowners relocating

Relocation timelines don’t always align with traditional home sale timelines. If your transfer date is firm and you need certainty, Sell Dave Your House offers Detroit-area homeowners a direct cash offer within 24 hours, with closing in as little as seven days.

There are no agent commissions, no repair requirements, and no waiting for an outside buyer to secure financing. Sell Dave Your House buys homes as-is, which means you skip the prep work and focus on your move. With over 16 years of experience helping homeowners in difficult situations, the team understands that relocation is time-sensitive. If you’re ready to get a cash offer or want to understand why homeowners sell fast, Sell Dave Your House is ready to help you close on your schedule.

FAQ

What is the relocation home sale process?

The relocation home sale process is a structured method where a relocation management company purchases your home from you and resells it to an outside buyer in two separate transactions, keeping employer assistance tax-free under IRS Revenue Ruling 2005-74.

What is a Buyer Value Option in relocation?

A Buyer Value Option (BVO) is the most common employer-sponsored program where you find an outside buyer, the relocation company purchases your home at that buyer’s price, and then resells it to the buyer in a separate transaction to avoid taxing the benefit as employee income.

How long does a relocation home sale take?

Most BVO transactions close within 60 to 90 days of listing, though the timeline depends on local market conditions and how quickly you engage your relocation management company after receiving your transfer notice.

What is the difference between BVO and GBO?

A BVO sets the purchase price based on an outside buyer’s market offer, while a GBO locks in a fixed price regardless of market conditions. Employers generally prefer BVO for cost control; employees often prefer GBO for the price certainty it provides.

Do I pay taxes on relocation home sale assistance?

Under a properly structured BVO or GBO program governed by IRS Revenue Ruling 2005-74, your employer’s home sale assistance is treated as a business expense, not taxable income to you, as long as the two transactions remain legally separate.