Why Cash Offers Suit Quick Timelines for Home Sellers

TL;DR:

- A cash offer in real estate allows homeowners to sell quickly without mortgage delays, often closing in 7 to 21 days. It removes financing contingencies, including loan underwriting and appraisal steps, making the process faster and more reliable. Cash buyers, especially investors and iBuyers, offer scheduling flexibility and are ideal for urgent financial needs or avoiding deal failures.

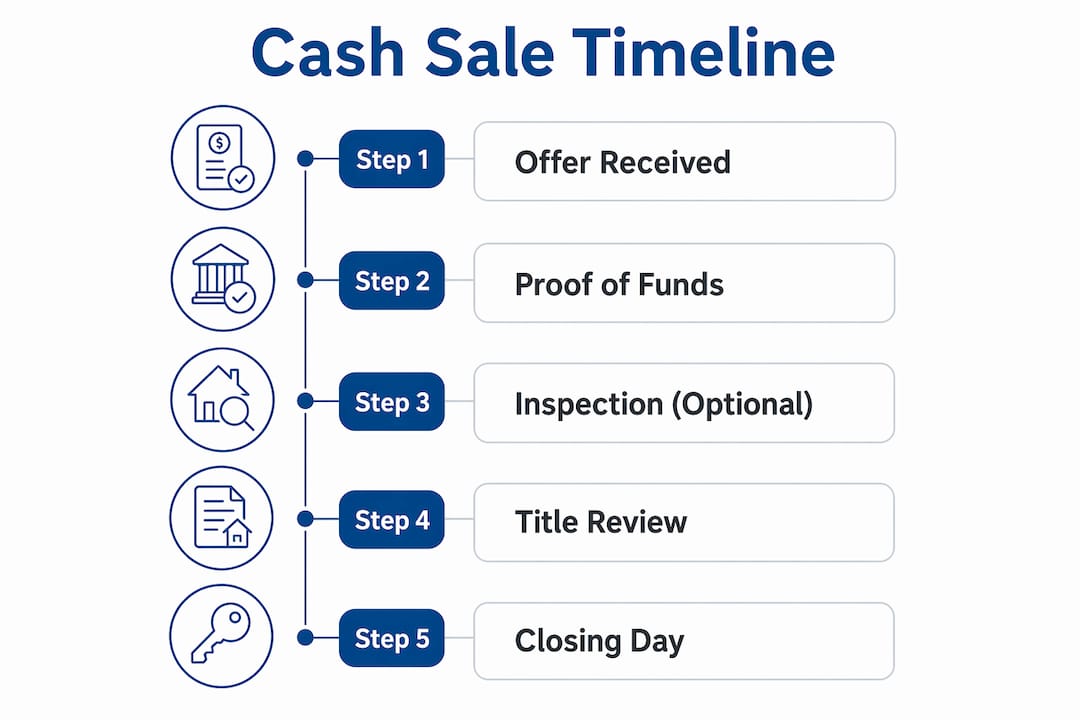

A cash offer in real estate means a buyer purchases your home without mortgage financing, removing the single biggest source of closing delays. That definition explains why cash offers suit quick timelines better than any financed deal: no lender, no underwriting, no waiting. Cash offers can close in as little as 7 to 21 days, compared to 30 to 60 days or more for mortgage-backed transactions. For homeowners facing foreclosure, a job relocation, divorce, or a sudden financial hardship, that difference is not a minor convenience. It is the difference between relief and prolonged stress.

Why cash offers suit quick timelines: the mechanics explained

The speed of a cash sale comes directly from what gets removed. A traditional financed sale requires a lender to verify the buyer’s income, pull credit reports, order an appraisal, and complete underwriting before issuing a loan commitment. Each of those steps adds days or weeks to the process, and any one of them can collapse the deal entirely.

Cash deals eliminate all of that. The buyer already has the funds. The closing process shrinks to title search, document preparation, and fund transfer. That is why fewer contingencies in cash offers translate directly into a faster, simpler closing.

Here is what a cash sale removes compared to a financed sale:

- Loan underwriting: No lender review of the buyer’s debt-to-income ratio or credit history.

- Appraisal contingency: No requirement for a licensed appraiser to confirm the home’s value.

- Financing contingency: No clause allowing the buyer to exit if their loan falls through.

- Mortgage approval delays: No waiting on a bank’s internal processing queue.

- Lender-required repairs: No list of fixes demanded before a loan will fund.

Pro Tip: Ask any cash buyer to provide a proof of funds letter from their bank before you accept an offer. This one step confirms the buyer can actually close and protects you from wasting time on an unqualified offer.

Real estate brokers consistently note that shorter closing schedules signal serious buyers, which sellers interpret as safer and more reliable deals. When a buyer can close in ten days, they have nothing to hide and no financing risk hanging over the transaction.

| Closing factor | Financed sale | Cash sale |

|---|---|---|

| Loan underwriting | 2–4 weeks | Not required |

| Appraisal | 1–2 weeks | Usually waived |

| Financing contingency period | 3–5 weeks | Not applicable |

| Typical total closing time | 30–60 days | 7–21 days |

What closing timelines look like for different cash buyers

Not all cash buyers move at the same speed. Understanding who is making the offer helps you set realistic expectations and choose the right fit for your situation.

Investors close the fastest, typically in 7–14 days. They buy properties as-is, skip inspections in most cases, and have funds ready to deploy immediately. The trade-off is price. Investors build profit margins into their offers, so you will generally receive less than market value. For homeowners who need to move quickly and cannot afford months of carrying costs, that trade-off often makes sense.

iBuyers (technology-driven buying platforms) offer a middle ground. Their timelines typically run 14–60 days, and they tend to offer prices closer to market value than traditional investors. However, they charge service fees that can reduce your net proceeds, and they are selective about which properties they purchase. Not every home qualifies.

Individual cash buyers are the most variable category. A private buyer paying cash might close in two weeks or might need six. Their timeline depends on personal circumstances, not a business model built around speed.

Key questions to ask any cash buyer before accepting an offer:

- How quickly can you provide proof of funds?

- Do you require an inspection contingency?

- Can you accommodate my preferred closing date?

- Have you closed cash transactions in this market before?

Cash buyers offer scheduling flexibility, meaning you can often negotiate the exact closing date to fit your move-out timeline. That flexibility is a real advantage when you are coordinating a relocation or waiting on a new home to become available.

How do cash offers help sellers with urgent financial needs?

Sellers facing urgent situations get the most from a fast cash sale. The benefits go beyond just speed.

Reduced risk of deal collapse is the most underrated advantage. Cash offers reduce the risk of deal failure because there is no financing contingency that can be denied at closing. With a financed buyer, a last-minute loan denial sends you back to square one after weeks of waiting. With a cash buyer, that risk disappears.

Faster access to sale proceeds matters enormously when you are behind on mortgage payments, facing medical bills, or managing an inherited property you cannot afford to maintain. A 10-day closing puts money in your account weeks before a financed deal would even reach the appraisal stage.

Fewer seller obligations make the process less exhausting. Cash buyers, particularly investors, purchase homes as-is. You do not need to repaint, replace appliances, or fix the roof before listing. That saves both time and money you may not have.

Situations where the advantages of cash transactions are clearest:

- Probate sales: Estates often need to liquidate property quickly to settle debts or distribute assets among heirs.

- Pre-foreclosure: Selling fast for cash stops the foreclosure clock and protects your credit from further damage.

- Relocation: A job offer in another city does not wait for a 60-day mortgage closing.

- Divorce: Both parties often want a clean, fast resolution rather than months of co-ownership.

- Downsizing: Retirees moving to smaller homes benefit from a quick, uncomplicated sale.

Pro Tip: If you need to stay in your home for a few weeks after closing, ask your cash buyer about a leaseback arrangement. Many investors and direct buyers will agree to let you rent the property back briefly, giving you time to move without pressure.

Sellers facing urgent financial or lifestyle changes find cash offers particularly valuable for quick relief, even when the price is slightly below what a financed buyer might offer after months on the market.

What trade-offs should you expect with a fast cash sale?

A cash sale is not a perfect solution for every homeowner. Knowing the trade-offs upfront helps you make a clear-eyed decision.

Price concessions are real. Sellers often accept 5–15% below market value in exchange for the speed and certainty that cash offers provide. That discount reflects the buyer’s risk, the as-is condition of the sale, and the convenience premium you are receiving. Before you decide, calculate what a traditional sale would net after agent commissions (typically 5–6%), repair costs, carrying costs during the listing period, and potential price reductions after inspection.

Proof of funds verification is non-negotiable. Verifying a buyer’s proof of funds is critical to confirming offer legitimacy and avoiding scams. Fraudulent cash offers exist. A legitimate buyer will provide a recent bank statement or letter from a financial institution without hesitation.

Additional considerations before accepting a cash offer:

- Research the buyer’s track record. Ask for references from previous sellers or check online reviews. A reputable cash buyer has a history of closing on time.

- Read the contract carefully. Even cash deals include terms. Watch for clauses that allow the buyer to renegotiate after inspection.

- Compare multiple offers. Getting two or three cash offers gives you a baseline and negotiating leverage.

- Weigh speed against net proceeds. If your home sold at full market value in two weeks on the open market, a cash offer at a steep discount may not be worth it. If your home needs significant repairs or you face urgent financial pressure, the math often favors cash.

The core question is straightforward: how much is speed and certainty worth to you right now? For many homeowners, the answer is quite a lot.

Key Takeaways

Cash offers are the fastest and most reliable path to closing for homeowners who cannot afford the delays, contingencies, or deal-collapse risk of a financed sale.

| Point | Details |

|---|---|

| Cash closes faster | Cash deals close in 7–21 days versus 30–60 days for financed sales. |

| Fewer contingencies | No appraisal or financing contingency means fewer reasons for a deal to fall apart. |

| Buyer types vary in speed | Investors close in 7–14 days; iBuyers take 14–60 days; individual buyers vary widely. |

| Price concessions are typical | Expect offers of 5–15% below market value in exchange for speed and certainty. |

| Verify funds before accepting | Always request proof of funds to confirm the buyer can actually close. |

What I’ve learned from watching sellers choose cash over financed offers

After years of working in real estate, the pattern I see most clearly is this: sellers who regret a cash sale almost always regret it for the wrong reason. They focus on the price gap and forget to count what a traditional sale actually costs them.

A homeowner carrying two mortgage payments for three months while waiting for a financed buyer to close is not saving money by holding out. They are spending it, slowly, while also absorbing the emotional weight of an unresolved sale. Certainty has real financial value, and most sellers underestimate it until they have lived through a deal that collapsed at the finish line.

The sellers I have seen benefit most from cash offers are not always in financial crisis. Some are simply people who value their time and peace of mind. A clean, fast closing lets them move forward. That is worth something that does not show up in a price comparison spreadsheet.

My honest advice: get a cash offer first, then list on the open market if the gap is too large. Knowing your cash floor gives you confidence and a backup plan. Most sellers who do this end up taking the cash offer anyway, once they see the full picture.

— Real Estate Team

How Sell Dave Your House makes fast cash sales straightforward

Sell Dave Your House has spent over 16 years helping Detroit-area homeowners close quickly, without repairs, agent fees, or uncertainty.

The process is direct. You contact Sell Dave Your House, share basic details about your property, and receive a fair all-cash offer within 24 hours. If you accept, closing can happen in as little as seven days. There are no commissions, no hidden fees, and no requirement to fix anything before the sale. Whether you are facing foreclosure, managing an inherited property, or simply need to move fast, Sell Dave Your House provides a clear path forward. Learn how the cash sale process works or get a cash offer today.

FAQ

How fast can a cash home sale actually close?

Cash sales close in as little as 7 to 21 days, compared to 30 to 60 days for mortgage-backed transactions. The exact timeline depends on the buyer type and how quickly title work is completed.

Are cash offers always lower than financed offers?

Cash offers typically run 5–15% below market value, but that gap often narrows when you subtract agent commissions, repair costs, and carrying costs from a traditional sale’s net proceeds.

What makes cash offers safer for sellers?

Cash offers eliminate financing contingencies, which are the most common reason deals fall apart at closing. With no lender involved, the buyer cannot be denied a loan at the last minute.

Do I need to make repairs before a cash sale?

Most cash buyers, particularly investors and direct buyers like Sell Dave Your House, purchase homes as-is. You are not required to make repairs, clean out the property, or stage it for showings.

How do I know if a cash buyer is legitimate?

Request a proof of funds letter from the buyer’s bank before signing any agreement. A verified proof of funds confirms the buyer has the money available and is serious about closing.